- News

- Women

- Magazine

- IndustryIndustry

- InsightsInsights

- Success Stories

- PublishPublish

- ContactContact

- Media KitMedia Kit

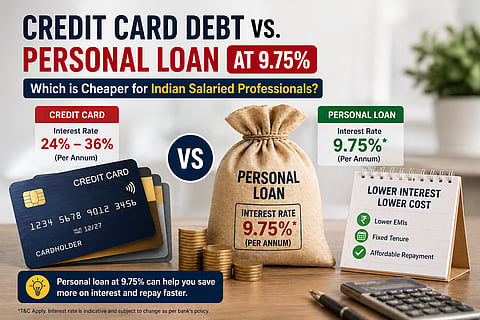

Credit Card Debt vs. Personal Loan

Credit Card usage among Indian salaried professionals has increased due to convenience and ease of access. However, unpaid balances often lead to high interest costs over time. Many borrowers compare this with a Personal Loan, which offers a defined interest rate, such as 9.75% per annum, subject to eligibility. A clear comparison of these options helps identify which one reduces total repayment and supports better financial planning.

A Credit Card allows borrowing up to a pre-approved limit, but unpaid balances incur interest charges. This interest compounds over time, increasing the total amount payable. Extended use without full repayment can significantly raise the cost of borrowing.

Several factors contribute to the increasing cost of Credit Card debt:

Interest compounds on outstanding balances and increases dues regularly.

Minimum payments reduce only a small portion of the principal amount.

Late payment fees apply when payments are missed or delayed.

These factors indicate that carrying balances over time results in a higher overall financial burden. Consistent monitoring of dues and timely repayment remain essential.

A Personal Loan provides a fixed amount that is repaid through equal monthly instalments (EMIs) over a defined tenure. This ensures clarity on repayment obligations and timelines. Such loans feature a fixed repayment term, which supports better financial planning and cost visibility.

The following features define how such loans function:

The interest rate on a Personal Loan remains fixed throughout the tenure.

EMIs remain consistent, which supports predictable budgeting.

A fixed tenure provides a clear repayment timeline.

Each EMI reduces the principal amount in a systematic manner.

These features provide stability and ensure repayments follow a structured and predictable path.

The key difference between these options lies in how interest is calculated and how repayments are planned. Credit Cards charge interest on outstanding balances, often at higher rates, while Personal Loans apply a fixed rate over a defined tenure. A loan priced at 9.75% per annum, subject to eligibility, is typically lower than the effective annual rates associated with Credit Cards.

EMI payments gradually reduce the outstanding principal. In contrast, Credit Card balances may remain high when only minimum payments are made. A lower interest rate on a Personal Loan, combined with a fixed repayment tenure, can reduce the total borrowing cost compared to long-term revolving credit.

Switching to a Personal Loan may be considered when Credit Card dues become difficult to manage. Consolidation allows multiple liabilities to be combined into a single repayment structure, improving cost control and repayment clarity. This approach becomes relevant in the following situations:

A borrower chooses to apply for a Personal Loan to clear high-interest Credit Card balances.

A borrower decides to get a Personal Loan to combine multiple dues into a single EMI.

Multiple Credit Cards create complexity due to different billing cycles.

Fixed EMIs replace variable payments and improve repayment discipline.

These situations highlight how consolidation can simplify financial obligations and reduce repayment uncertainty.

Before considering a switch, it is important to assess eligibility for a Personal Loan. Lenders evaluate specific criteria to determine borrowing suitability. For instance, Personal Loans offered by HSBC Bank require applicants to meet defined income and profile requirements. These checks ensure that repayment capacity aligns with the loan structure.

Common requirements include:

Age within a defined working range, usually 21 to 60 years.

Stable employment and a regular source of income.

An existing banking relationship, such as an active account.

Availability of identity, address, and income documents.

Meeting these conditions improves the chances of approval and ensures a smoother application process.

The decision depends on repayment behaviour and total cost over time. Credit Cards serve short-term needs effectively when balances are cleared within the billing cycle. However, unpaid balances increase costs due to compounding interest.

A Personal Loan offers a fixed repayment tenure with predictable costs. When repayments stretch over a longer period, a fixed-rate loan makes the total cost more predictable and easier to manage. A careful comparison of overall costs helps identify the more economical option.

A Personal Loan at 9.75% per annum, subject to eligibility, generally offers a more cost-efficient option than maintaining long-term Credit Card debt. Credit Card balances can increase due to compounding interest and extended repayment periods. In contrast, a Personal Loan provides a fixed repayment structure with clear timelines and predictable instalments. A detailed comparison of both options enables salaried professionals to select a solution that supports financial stability and effective debt management.

Follow us on Google News